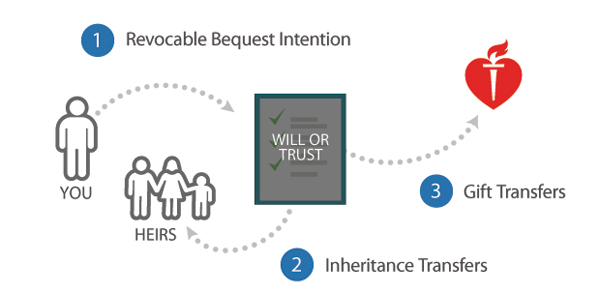

Will or Trust

About This Gift

Your will gives you peace of mind knowing that loved ones are taken care of, your assets are distributed accurately, and that your gift to the association reflects your personal values. Gifts to charitable organizations are excluded from estate tax.

How It Works

- You can provide now for a future gift to the American Heart Association or American Stroke Association by including a bequest provision in your will or revocable trust.

- Your will or trust directs assets to your heirs.

- Your will or trust directs a bequest to the American Heart Association or American Stroke Association for the purpose(s) you specify.

Benefits

- Your assets remain in your control during your lifetime.

- You can modify your bequest if your circumstances change.

- You can direct your bequest to a particular purpose (be sure to check with a Charitable Estate Planning Representative to make sure your gift can be used as intended).

- There is no upper-limit on the estate tax deductions that can be taken for charitable bequests.

- You can have the satisfaction now of knowing that your bequest will support the association in the way you intended.

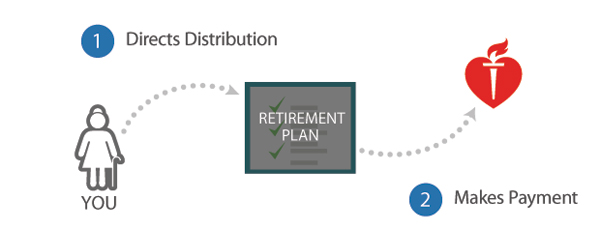

Retirement Plan Assets

About This Gift

It is important to review retirement accounts, such as IRAs, 401(k)s, 403(b)s, or other retirement plans periodically. Due to high tax rates, many supporters have found that it makes financial sense to allocate the residual amount of their retirement savings to the association. The association does not pay tax on these gifts, and can put every dollar of your gift to work in the fight against heart diseases and stroke.

How It Works

- You name the American Heart Association or American Stroke Association as the sole or partial beneficiary of your IRA, 401(k), or other qualified plan using the beneficiary designation form provided by your financial institution.

- You continue to make withdrawals from your account during your lifetime. Any residual left in your account after passing will flow to the association tax-free according to your allocation on your beneficiary designation form.

Benefits

- You can escape both income AND estate tax levied on the residual left in your retirement account by leaving a gift to the association because we are a non-profit organization and do not pay taxes on the transfer. These taxes can eat up the principal of your account when transferred to your heirs.

- You can continue to take withdrawals during your lifetime.

- You can designate all or a percentage of your account and can change your beneficiaries at any time. There is no charge to update your beneficiary form.

Qualified Charitable Distribution

About This Gift

Also commonly known as an IRA Charitable Rollover gift. Donors age 70 ½ and older may direct lifetime distributions from their traditional or Roth IRA to the American Heart Association or American Stroke Association. This distribution may* count toward your required minimum distribution without increasing your taxable income. You can make contributions totaling up to $100,000 to the association and other qualified charities annually.

*If you make contributions to your IRA after age 70 ½, some charitable distributions from your IRA may be treated as income. Please discuss this with your financial advisor before contributing.

How It Works

- Notify your IRA custodian to make a direct transfer of the distribution amount from the IRA to the American Heart Association or American Stroke Association.

- You take the portion of your required minimum distribution (RMD) that you need as income and transfer the remainder to a qualified charity, thereby only paying income tax on the needed income*.

- Obtain a written acknowledgment from the qualified charity (different from a tax deduction receipt) to benefit from the tax-free treatment.

Benefits

- The distribution counts toward your required minimum distribution (RMD).*

- You effectively bypass paying any income tax* on the amount transferred to charity versus if you take your full required minimum distribution (RMD), paying tax on the income and then writing a check to a charity.

-

Up to $100,000 of the amount transferred qualifies for this beneficial tax treatment.

Testamentary Charitable Gift Annuity or Testamentary Charitable Remainder Trust

About This Gift

As of January 1, 2020, non-spousal beneficiaries of your IRA must take all distributions from the account within ten years unless they meet the exceptions of being a minor child, disabled, chronically ill, or a person not more than ten years younger than the account owner. Making a Charitable Gift Annuity or Charitable Remainder Trust the beneficiary of your IRA allows for fixed payments to your non-spousal beneficiaries (i.e., children or grandchildren) over a longer span of time.

How It Works

- Your estate plan specifies the gift vehicle, income beneficiaries, charitable remainder beneficiaries and amount of your IRA to fund the vehicle upon your passing.

- With a Charitable Gift Annuity your chosen income beneficiaries will receive income for life. Or, with a Charitable Remainder Trust your beneficiaries will receive income for life or a term of years.

- At the end of the life/lives/term, the remainder passes to your chosen charity.

Benefits

- Your non-spousal beneficiaries do not have to take the entire distribution from your IRA within ten years. This could help your beneficiaries from being pushed into a higher income tax bracket with a very large tax bill.

- You can protect your IRA from beneficiaries who might deplete the account quickly by specifying the term they receive fixed payments.

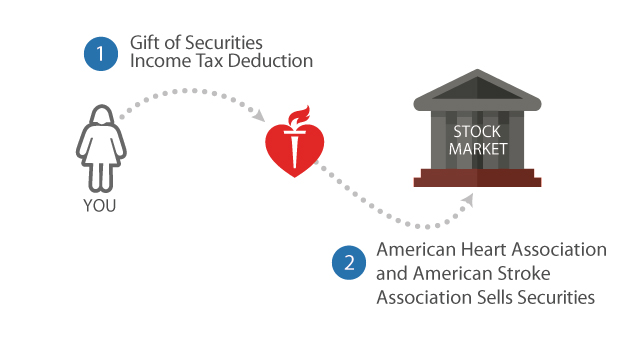

Stocks, Bonds, Mutual Funds

About This Gift

You have worked hard all of your life to grow your investments. There are many ways to make your investments work for you. Maximize your monetary gain by funding a charitable gift with donated appreciated stock, mutual funds, or bonds. This is a tax savvy way to help benefit the world in future years to come.

How It Works

- You transfer securities to the association.

- The association sells your securities and uses the proceeds for important programs such as research, quality care, community outreach, educating the world, and our reach expands every day.

Benefits

- You receive an immediate tax deduction for the fair market value of the securities on the date of transfer, no matter what you originally paid for them.

- You pay no capital gains tax on the securities you donate.

- You can direct your gift to a specific fund or purpose.

Ready to donate? Call

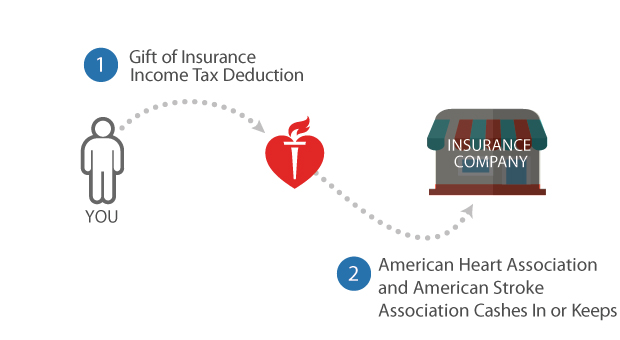

Life Insurance

About This Gift

You can use a life insurance policy that is no longer needed to show your support in our fight against heart disease and stroke. If you want to keep your current policy but make a future gift, you can leverage your policy by simply naming the association as a beneficiary of your policy.

How It Works

- You transfer ownership of a paid-up life insurance policy to the association.

- The association elects to cash in the policy now or to keep the policy and receive the life benefits later.

Benefits

- You receive an immediate income tax deduction for the cash value of the policy.

- In some cases, you can use the cash value in your policy to fund a gift that pays you income.

- You have the satisfaction of making a significant gift now to the association without adversely affecting your cash flow.

Real Estate

About This Gift

You can give a gift of your vacation home, commercial property, or undeveloped land to the association. These properties can be donated towards our cause as an outright gift or can be used to fund a gift that pays you a lifetime of income.

How It Works

- You will need to obtain a philanthropy title report and an independent review.

- Our advisors will inspect the property and complete an environmental checklist.

- The IRS requires an independent appraisal to establish the fair market value of the property. We can assist you in following the IRS procedures.

Benefits

- You may apply the deduction for up to 30 percent of your adjusted gross income, and carry it forward for up to five additional years.

- You are freed from paying real estate taxes, maintenance costs, insurance, and capital gains taxes on the property’s appreciation.

- You also remove the asset from your taxable estate.

- To review your gift possibility and evaluate the condition and marketability of the property contact a Charitable Estate Planning Representative.